Networked devices. Ubiquitous connectivity. Cloud computing. Social networks. Near Field Communication… as powerful forces combine to connect nearly everyone to practically everything, Payments will be revolutionized in ways no one can clearly foresee.

Right now major card issuers, mobile operators, payment networks, technology companies and device manufacturers are all vying to shape what comes next. The stakes are huge. Mobile Payments is increasingly the key to commanding customer relationships, in mature economies as well as emerging markets.

Who will shape Mobile Payments? Talent will tell.

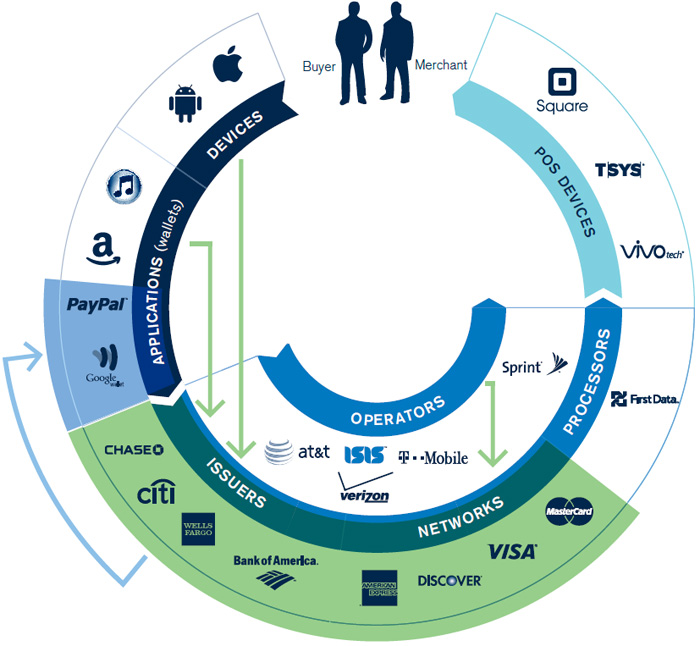

Ecosystems

The mobile technology required to revolutionize Payments already exists. The critical challenge now is converting technological possibility into market-leading capability – i.e., create and deliver Mobile Payments solutions that customers and merchants will embrace. The challenge is far from uniform. Payments “ecosystems” vary greatly around the world.

In developing countries, the most compelling Mobile Payments opportunities are banking the unbanked and digitizing cash. (Over 90% of transactions worldwide are still cash-based). In the more developed, wealthier markets where cashless transactions are already the norm, the big opportunity is revolutionizing the buying experience. “Mobile Payments isn’t about how you are going to pay, but what you are going to buy and where,” said Ryan Hughes, Chief Marketing Officer of the Isis joint venture (AT&T, T-Mobile USA, and Verizon Wireless) in his remarks at the 2012 Mobile World Congress in Barcelona, Spain.

Amazon pointed the way. Not only does the pioneering online merchant offer consumers a vast array of choices, it also recognizes and welcomes each buyer who signs into their site, and offers them personalized recommendations based on individual and collective buyer behaviors. Mobile Payments will take such transactional data exchange to new heights, creating unprecedented intimacy between consumers and merchants. Sellers will know who their buyers are, where they are, and what they want – data they can use to cater to customer preferences and command their loyalty. As Citi’s Chief Operations & Technology Officer Don Callahan stated at the 2012 Mobile World Congress: “Information about money is at least as important as money itself.”

“The real value comes when you receive offers and information based on who you are and what you want at precisely the right moment,” said Isis CEO Michael Abbott, in his Mobile World Congress keynote address. “Retailers can now connect with customers when they walk in the door, not like today when they are at the checkout about to walk out. And you have a channel for delivering relevant offers at the moment of retail truth, when information meets intent and purchasing decisions are truly made.”

To date, progress toward grand visions of what Mobile Payments can become remains highly uneven. Mobile Payments ecosystems are advancing at different rates around the world. The vertically integrated markets of Japan and South Korea, for example, are visibly leading, especially in mobile contactless payments for transit and convenience purchases, while the US and Europe mostly lag behind.

The US ecosystem seems especially poised for innovation. This vast, wealthy market has no monopolies in telecom or banking to drive a single Mobile Payments standard. The relative freedom (and thus confusion) of the North American market has probably slowed Mobile Payments progress thus far, as has the existing predominance of cashless transactions, making the value-add of Mobile Payments less compelling to many merchants and consumers. Of course, we have seen the pattern before. The US market was comparatively slow to adopt cellular phone use in the 1990s. A decade later, cell phones were everywhere.

Some industry observers suggest that the advance of Mobile Payments in North America will continue its halting pace, but others foresee more rapid progress. In his address to the Mobile World Conference, Google Executive Chairman Eric Schmidt noted that new consumer experiences such as buying and reading books online, automated translation of languages, and computer voice recognition all became reality much faster than was forecast. His implication? Mobile Payments could become a much bigger part of American consumers’ everyday experience much sooner than experts foresee.

Perhaps. But in a market lacking structured vertical integration, the advance of Mobile Payments will stem from the voluntary and often problematic collaboration of widely disparate players, among them card issuers, payment networks, mobile operators, applications, and device makers. These strikingly dissimilar businesses must now find ways to join together to creatively craft practical, secure, and differentiated Mobile Payments solutions.

“It’s exciting and it’s daunting,” commented Marc Keller, Citigroup’s Global Director of Digital Networks & Mobile, speaking at the Mobile World Conference. “There are the challenges of customer and data ownership. But just look at what Starbucks has done…. A gift card, loaded on a phone. That 26 million transactions were made in one year shows there is customer curiosity about this.”

Transcendent Teams

In relatively free markets like the US, talent is the key competitive variable. The Mobile Payments space will be shaped not by government mandate or staid boards setting industry standards, but by visionary executives leading diverse teams whose collective knowledge and strategic insight transcend industry silos to take in the whole of the Mobile Payments landscape.

Who are these visionary leaders? Where are they now? What opportunities do they seek? What kinds of corporate cultures will best nurture their abilities? What skills and traits will they look for as they build their teams?

This paper explores the race to form top-level teams with the right stuff to lead the marketplace. Our base research scanned relevant executive talent trends across nine companies, all noteworthy contenders in North American Mobile Payments:

1. Visa

2. American Express

3. MasterCard

4. Citigroup

5. Wells Fargo

6. JP Morgan Chase

7. Bank of America

8. PayPal

9. Google

Specifically, we studied the path taken by more than 200 executives within these nine companies to their current positions on Mobile Payments teams. The picture that emerged from this scan was remarkably fluid. Talent is migrating in multiple directions across traditional industry boundaries to form Mobile Payments teams with diverse backgrounds. A few of the trends we identified: Card issuers and card networks (e.g. Wells Fargo, Citi, Chase, MasterCard, Visa) have been drawing talent away from high tech companies like Google and PayPal, as well as from mobile operators (e.g. T-Mobile, Verizon) and some mobile device companies. Similarly, Google and PayPal have crossed industry boundaries to draw talent away from card issuers.

Our research produced a snapshot of widespread talent migration that is clearly ongoing, as evidenced by the continuing stream of new hire announcements in the first quarter of 2012. Many Mobile Payments executives moved into their current positions in 2010 or 2011. Over a third of the executives in our sample moved across industries to their current jobs. Among those who migrated across industries, roughly half brought experience specifically in Mobile Payments. Others were selected for their functional expertise. In the first phase of the industry’s development, the skills in high demand were Strategy and Planning, because the focus was on ideation and prototyping. Currently there is a healthy demand for Product people, as well as people to carry Business Development and Marketing and Sales forward.

“Players in this space need to have expertise in direct-to-consumer distribution in addition to retail Payments experience,” observes Gaurav Zutshi, Senior Vice President and Global Head of Product Management at Obopay, which he joined in 2010 after a six-year stint at Visa International. “As Mobile Payments providers extend their consumer base, there is obvious demand for people who understand payment risk and fraud, who can use sophisticated analytics and are also able to serve new customer segments with effective use of social media for product marketing and inducing trial,” Zutshi adds.

“No doubt, big players in financial services are moving away from their traditional ‘hire-someone-from-financial services’ route, because so much of the technological expertise you need for Mobile Payments can only be found outside their industry,” notes Nitin Gupta, Regional Manager, North East at Yodlee. “But it’s not just about getting tech-savvy people. To lead them, you need an ‘evangelist’ – someone who understands Payments, mobile technology and customer experience with a passion. Especially for the more senior roles, you need individuals with the vision and knowledge to make new technology fit customer needs.”

While card issuers and payment networks appear to be relative aggressors in crossing industry boundaries to secure a more varied mix of executive talent than can be readily found within their own ranks, all the companies we studied have drawn at least some key talent from settings quite different from their own.

In February 2010, Visa tapped Bill Gajda, formerly Chief Commercial Officer at GSMA (an association of mobile operators promoting the GSMmobile standard) as its new Global Head of Mobile Product, with a charge to “further advance Visa’s mobile strategy, working in collaboration with the wireless and financial services industries to bring mobile payments and related services to consumers around the globe.” Visa also brought back Jennifer Schulz, then CEO of Verifi, to be its Head of Global Product Strategy, Innovation and eCommerce. Today, Schulz is visibly in charge of Visa’s most significant bet in Mobile Payments, the new “V.me” digital wallet.

Payfone, which advocates for checkout processes based on carriers’ information on their consumers, is backed by American Express, Verizon and Rogers Communications, and is led by a team with solid operator experience. In March 2012, it announced that it had attracted three payments veterans to its team: Prakash Hariramani joins as VP, Head of Product from Visa, where he drove execution for the Visa digital wallet. William Murray joins as VP of Financial Institution Sales from MasterCard Worldwide, where he was responsible for initiating MasterCard’s merchant-focused eCommerce strategy. And Amy Masters joins as Director of Marketing from American Express.

Citi, Chase, and MasterCard have all hired key Payments executives away from PayPal. In June 2010, Chase announced that Jack Stephenson – formerly PayPal’s Senior Vice President of Strategy, Partnerships, Analytics and New Ventures – would join Chase as Managing Director of Mobile, E-Commerce and Payments, with responsibility for leading “the continuing evolution and implementation of a company-wide strategy for mobile devices and internet payments.” Dickson Chu, who recently joined LivingSocial as Senior Vice President for Merchant Solutions, had left PayPal just two years before to be Head of Digital and Mobile for Citi.

PayPal has several times returned the favor, tapping key talent from issuers and payment networks. In September 2009, PayPal hired Ed Eger, Citigroup’s CEO of International Cards, to be its Senior Vice President and General Manager of North America. Eger is responsible for establishing PayPal as “the preferred online payment method for consumers and merchants in the U.S. and Canada,” and for overseeing PayPal’s global core payment processing. More recently, PayPal hired Rupert Keeley, who was then President for the International businesses of Visa, to run its Payments business in the Asia Pacific market.

Further signs of PayPal’s determination to dominate in Mobile Payments include the March 2011 hiring of Don Kingsborough, founder and CEOof Blackhawk, Safeway’s prepaid card network. As Vice President for Retail and Prepaid Products, Kingsborough will lead PayPal’s charge into traditional retail environments, enabled by Mobile Payments. PayPal also beefed up its capabilities by acquiring Zong, whose technology allows online gamers and others to make micropayments on the Internet if they have a postpaid mobile phone.

American Express has tapped key talent from mobile operators and elsewhere. In 2010, Dan Schulman – formerly President of the Sprint Nextel Prepaid group – joined Amex as Group President, Enterprise Growth, with responsibility for “the company’s global strategy to expand alternative mobile and online payment services, form new partnerships and build revenue streams beyond the traditional card and travel businesses.” Many of the team members Schulman initially recruited to Amex were also drawn from mobile operators.

Nevertheless, it would be a mistake to assume that American Express sought Schulman only for his Sprint Nextel experience. “Experience with a mobile operator is not the most crucial consideration when putting together a great Mobile Payments team,” suggests Bharathi Ramavarjula, who is currently the Senior Director of E-Commerce and Mobile Payments at Walmart.com, and previously held Payments positions at Visa, Microsoft, and Amazon. David Schwartz, Obopay’s VP of Product and Corporate Marketing, concurs. “Mobile operator experience is not as critical in the US as in some other major markets, such as India or in Kenya,” he says. “Having experience with technology innovation, particularly in Payments, carries more weight.”

Many believe that the innovative, visionary thinking required to lead Mobile Payments in North America can be more readily found in the other silos that span the ecosystem. “Telcos aren’t exactly the paragons of innovation. We do need to change that,” acknowledged René Obermann, CEO of Deutsche Telekom, in his Barcelona conference address. Obermann recently added “Product and Innovation” to his list of formal CEOresponsibilities. “If you want to transform your company, you must lead the change effort,” Obermann explained.

It seems likely American Express wanted Dan Schulman less for his experience working for a mobile operator than for his track record as a “technology evangelist.” Before joining Sprint, Schulman was the founding CEO of Virgin Mobile USA, where he led the company from its concept stage and national launch in 2002 to become one of the nation’s top wireless carriers. Before that, he was CEO of Priceline.com. A blog recently posted by JJ Hornblass reported that while Schulman may have recruited heavily from mobile operators early on at Amex, he had recently stocked his American Express team with ex-Google and ex-startup programmers. Schulman told Hornblass that as he was walking an Amex colleague through his team’s work space, the colleague said: “Lots of tattoos here.” “There are,” Schulman agreed. “We are trying to develop a whole different way of thinking in the company.”

Google, never shy in any contest, has crossed industry lines in several instances, drawing some of its Mobile Payments team members from Deutsche Bank, Amex, and PayPal, among others. In the first half of 2011, Google hired away two PayPal executives with Mobile Payments expertise – Stephanie Tilenius and Osama Bedier. PayPal subsequently filed lawsuits against both the executives and Google. In December 2011, Peter Hazlehurst joined Google as Global Head of Payments, moving over from Yodlee, a Northern California software company whose account aggregation service allows users to see their credit card, bank, investment, email, travel reward accounts, and other key information all on one screen.

Some of the more innovative and entrepreneurial evangelists will likely never join a big company, preferring to build and create their own platform. One example is Jack Dorsey, who created Twitter while studying at NYU. Dorsey launched Square in 2009 and still leads it as CEO. Square is a small square-shaped device that allows individuals and very small businesses (e.g. taxi drivers) to accept debit and credit cards by swiping the card on a reader attached to their mobile phone.

Strategic Capability

The stakes in the contest to shape the future of Mobile Payments are so staggeringly high, it is not surprising that many companies are experimenting with multiple approaches for building strategic Mobile Payments capability. It is a multi-industry game of musical chairs, in which everyone is trying to find their place. Our scan observed three main strategies:

1. Aggressively attract key team members, one at a time

2. Acquire existing teams, intact

3. Form strategic partnerships

American Express has notably blended all three: aggressively recruiting individual executives; acquiring Revolution Money in 2010; and signing on as a partner to the Isis joint venture, whose other card partners now include Visa, MasterCard, Discover, BarclayCard, Capital One, and Chase. Similarly, PayPal has acquired Zong in addition to hiring Ed Eger (Citigroup) and Rupert Keeley (Visa) to fill strategic leadership roles.

In 2011, Visa announced that it was acquiring Fundamo, a privately-held, Cape Town, South Africa-based company whose platform enables the delivery of mobile financial services to unbanked and under-banked consumers. Also in 2011, Visa acquired Karl Mehta’s Santa Clara-based company PlaySpan, whose Payments platform handles transactions for online games, digital media and social networks. Visa had previously beefed up its cutting edge Payments capabilities with its 2010 acquisition of CyberSource which is strategically located in Mountain View, California and provides electronic payment, risk management and payment security solutions to online merchants.

Citi, Chase, BofA and Western Union have all moved strategic Payments teams from the East Coast to the San Francisco Bay Area, presumably to tap some of Silicon Valley’s legendary innovative spirit. A Silicon Valley presence provides proximity to a large pool of talent with experience in startups and deep understanding of commercial innovation, as well as an extensive supply of savvy Venture Capital talent. For similar reasons, Visa has maintained Fundamo’s independent identity, preserving the young South African firm’s strong innovative culture.

Executive Competencies

Our scan of the rapidly evolving Payments space suggests that Mobile Payments executives will particularly need to demonstrate four of the key competencies Egon Zehnder assesses in standardized Management Appraisals for High Potentials:

Market Insight. Senior team members must have penetrating insight to discern what might happen in a complex, confusing, and fast changing environment.

Strategic Orientation. Mobile Payments leaders will face one strategic choice after another. Operational excellence alone will not get them far. Rather, they will have to shrewdly and correctly determine how their own company can get out front of the Mobile Payments industry, how to deliver a superior value proposition, what partnerships to form, etc.

Developing Organizational Capability. Mobile Payments leaders must attract diverse perspectives and richly varied forms of expertise to their teams. The ongoing challenge will be leveraging the team’s diverse strengths (see Team Effectiveness section below).

Change Leadership. Mobile Payments executive teams will need to be extraordinarily adaptive, nimble, and tolerant of uncertainty. PlaySpan’s Karl Mehta calls this ‘morphing ability’ – a combination of humility and agility.

Team Effectiveness

Securing these essential competencies – in addition to the requisite technical expertise – will require Mobile Payments teams to attract the best talent from across the industries that constitute the Mobile Payments ecosystem. Will a group of extremely talented individuals, brought together from diverse backgrounds, gel into an effective team? The answer is critically important, and anything but certain.

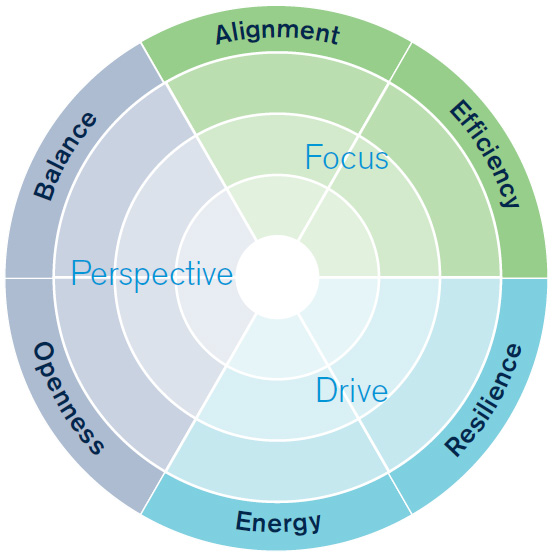

The talent level of the individuals a company attracts to its team is of course just one of the factors that determine team success. How the team interacts is at least as vital. Through years of research and experience with executive teams, we have identified six keys to team effectiveness:

Alignment. Shared beliefs and goals effectively focus the actions of all members.

Efficiency. The team optimizes resources to achieve results through calculated trade-offs and disciplined management processes.

Resilience. Mutual trust and respect support constructive resolution of issues and help the team perform well under pressure.

Energy. The team is energized by working together, is proactive and sustains momentum.

Openness. As it shapes and executes strategy, the team stays keenly attuned and responsive to the broader organization and outside world.

Balance. Within the team, diversity of relevant skills, styles and perspectives is valued and effectively leveraged.

Innovation Teams

In every team setting, all six dimensions are important, but certain strengths are especially important for certain kinds of teams. Mobile Payments teams must function predominantly as innovation teams, and they will work in an unusually fluid environment. As such, we believe Alignment, Energy and Openness will prove particularly vital.

Alignment is key because the most capable Mobile Payments teams will combine individuals with richly varied experience and contrasting styles. For example, the day Dan Schulman was introduced at a town hall meeting in buttoned-down American Express, a man strode into the auditorium and committed the double affront of wearing jeans and taking a seat in the front row – both no-no’s at CEO Town Hall sessions at that time. The arrival of this stranger sent a rustle of whispers through the auditorium. Was this casually-clad visitor unaware that he was at American Express? CEO Ken Chenault then took the stage, introducing the visitor as Dan Schulman, Amex’s new Group President, Enterprise Growth. The underlying message was clear: “Yes, he’s wearing jeans, but this is the executive who will lead us into the future.”

To achieve alignment, Mobile Payments teams must define a unifying higher purpose. The most powerfully aligning visions will have no bias toward any one industry’s point of view. Rather than transplant an existing model from a mobile operator, card issuer, device manufacturer or applications firm, winning Mobile Payments teams will innovate truly new strategies for leveraging technology to bring highly differentiated value to customers. The most oft-repeated phrases at the 2012 Mobile World Congress were “ecosystem” and “changing people’s lives.” This is evidence of nascent alignment beyond the turf wars that unavoidably arise when each industry defends its own agenda (e.g. operators pushing for the standardization of SIM-based NFC adoption). As Isis’ Michael Abbott noted, “The opportunity is vast. But rewards will be captured by none if not captured by all. For that we need to give customers choice, privacy, and simplicity.”

Energy is essential because the fast tempo and unpredictability of the Mobile Payments space will require teams to advance largely via constructive failures. To effectively pursue their innovation mission, Mobile Payments teams will need a culture that encourages idea fluency, “creative confidence” (a term coined by David Kelley, Chairman of IDEO), and high levels of “push” from all team members. The best Mobile Payments teams will be fueled by a sense of discovery, adventure and boldness.

Openness is a crucial counterbalance to both Energy and Alignment. As Mobile Payments teams align around shared goals and build momentum toward their fulfillment, the outside environment may suddenly shift. When it does, will the team shift in kind? Or will it ignore the new conditions and continue down the path for which all members feel a strong shared passion? To effectively steer, the team needs to stay close to changes in the environment and continuously adapt. As important, if a Mobile Payments team becomes too insular in its thinking and veers too far from the company’s overall direction, the larger corporate culture may reject it, just as the human body will reject any entity it deems too foreign. Successful innovation teams maintain their strong innovation culture as they also build effective bridges with the partners/organizations vital to commercializing their innovations.

In sum, it is essential that Mobile Payments teams stay attuned to changes in the marketplace, morph their direction accordingly, and remain in close communication with the ecosystems to which they belong, building-in inclusion by systematically connecting even with people beyond those who need to know what the team is doing.

Keys to Winning in Mobile Payments

Recognize that the talent of your Mobile Payments team will be a decisive competitive variable.

Know that Mobile Payments success demands more diverse kinds of talent than can be found solely within your own industry.

Entrust Mobile Payments leadership to executives who demonstrably excel in terms of Market Insight, Strategic Orientation, Developing Organizational Capability and Change Leadership.

Ensure your Mobile Payments team develops essential team competencies, especially Alignment, Energy and Openness.

Stay alert to shifts in the Mobile Payments landscape and be adaptive in your approach to developing strategic capabilit

Conclusion

It is often said that we tend to overestimate the speed with which new technology will be adopted, but we tend to underestimate its long term effects. Right now, every player in Mobile Payments has profound opportunity to influence what the space will look like a few years down the road. The game is clearly on, with tremendous activity expected in 2012 – partnerships, talent hirings, and the emergence of a large number of offerings (e.g. digital wallets are being developed by Google, Isis, Visa, and most issuers). Talent is pivotal. The players who shape the future of Mobile Payments will be those who view talent as a key competitive variable, clearly discern which competencies matter most in this fast changing arena, and successfully attract the very best talent from across the ecosystem.