Like other industries before it, financial services finally has awakened to the reality that it is not sheltered from the urgent need to rethink its business model, as well as the experience and engagement of its customers. Until now, there have been technology-driven developments in financial services such as online banking and more streamlined ways of conducting business, but these ultimately have been incremental, cosmetic improvements. They don’t fundamentally change the nature of banking and financial management in the way that other sectors (such as consumer retail) have leveraged mobile adoption to transform comparison, purchase and delivery of products and services.

The financial services industry has been able to survive on incremental change because the industry has existed in a walled garden, often protected by regulatory considerations and the scale of its key players. Potential competitors have been deterred by high barriers to entry, and consumers have been immobilized by high switching costs. But now those walls are collapsing, and the industry has become exposed to fast-moving market forces. A wave of entrepreneurial disruptors, as well as offerings from well-established “digital native” firms outside the banking industry such as Alibaba, Google, Lending Club, Simple and others, threaten traditional banks across the product spectrum from payment systems to wealth management. (Consider that in 2013 alone, Starbucks took in $4 billion in customer deposits through its Starbucks Card.) These new competitors are playing a completely different game and thus are able to deliver the intuitive, customized, on-demand experience that consumers have come to expect in everything they do and buy. Furthermore, the ability of these competitors to scale quickly means they can move from curiosity to marginal player to market leader faster than many legacy companies can respond.

Financial services companies now are in the cross hairs of transformation; it is their turn to adapt — quickly — or die. But addressing this threat can be more than an exercise in survival. It also is a pathway to enormous opportunity. In a customer-centered market economy, financial services is uniquely positioned to be the gatekeeper to valuable insights that reach to the core about how people live and aspire to live. This advantageous positioning is both structural and emotional; despite occasional commentary that suggests otherwise, the industry still holds the trust of the banked and unbanked population. But to seize that opportunity, financial services firms will need to attract and integrate into their organization top-tier digital leaders who can help lead the transformation of this highly regulated industry to a customer-led future.

To do so, financial services firms must compete for talent against not only each other but against the disrupting startups that seek to displace the “old guard,” as well as companies from other industries undergoing similar shifts. Compounding the challenge, financial services firms are at a disadvantage because of their reputation for being slow moving and adverse to innovation. However, the very magnitude of the task facing the industry can make it highly attractive to a particular cohort of leaders that thrives on the opportunity to disrupt established institutions, solve intractable problems and harness technology to improve the quality of life.

Turning talent challenges into strengths, however, requires a comprehensive strategy. Egon Zehnder has worked with dozens of financial services organizations in the Americas, Europe and Asia to help them build their digital capabilities. We have consistently found that successfully embracing customer centricity requires the following components:

Commitment from the top. Digital transformation never is a simple task. It is difficult to identify which path to take, and, once on that path, the journey rarely is straightforward. If the organization is going to reach a digital endpoint, the company’s Executive Committee must embrace this uncertainty as a company-wide issue; the transformation must be led by the business and those with P&L responsibility rather than siloed with someone like a chief innovation officer. Furthermore, conventional mediumterm planning often is of little help. Instead, the path forward must be discovered through a managed iterative process of trial and error. This in itself calls for a fundamental shift in the way these companies traditionally have been run.

Senior leadership also must support the fact that the transformation process is likely to involve some cannibalization of existing elements of the business. For example, more intuitive and accessible wealth management products may undermine traditional private banking offerings. Executives on the receiving end of those encroachments can be expected to fight these developments. The company’s CEO needs to make it clear to all involved that those leading the transformation have his or her personal support and commitment.

A customer-led vision to match the size of the task. Company leadership needs to recognize that, this time, incremental improvements will not be enough. This acceptance begins with a vision with the scale of true transformation. The goal is not, for example, to increase the company’s share of the mortgage market but rather to examine the mortgage experience from the bottom up and then rebuild it so that customers can be engaged through a product offering and with an experience tailored to needs they did not know could be addressed. After all, the real currency of the customer-centric world is the delight that flows from unexpectedly receiving something of value. A seasoned digital leader with deep product and analytics experience who is given a seat at the table can accelerate this process. He or she could come from a range of industries.

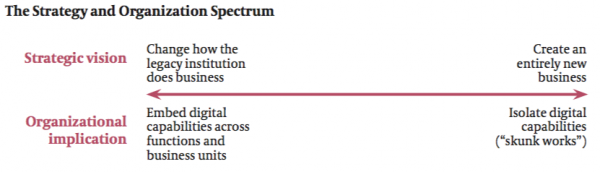

The right organizational structure. A company’s strategic vision for digital transformation then must be translated into a plan for deploying digital leadership within the organization. In looking not just at financial services but at other industries grappling with transformation, the options for the integration of the digital function can be thought of as defining a spectrum in which the strategic vision leads to an organizational implication (see Figure 1).

It is important to note that embedding digital capabilities across an organization must be done carefully. Even if the end goal is to have digital capabilities dispersed, they must begin concentrated in key areas, with enough critical mass to be able to achieve measurable success. That success then will provide a basis that allows for digital capability to spread.

Remember as well that a company’s digital strategy can change over time or that multiple strategies can be pursued simultaneously. As with so many things involving digital, there is no single prescriptive answer. But knowing where the organization’s transformation initiative sits on the spectrum provides clarity on the role requirements for digital leaders; for example, those who are embedded in the organization will need greater competency in collaboration and influence than those who are kept in an isolated “skunk works.” BBVA’s restructuring to put digital transformation at the center of its business, which it announced in a May 2015 press release, is a notable illustration of how organizational structure can be leveraged to help propel greater customer centricity.

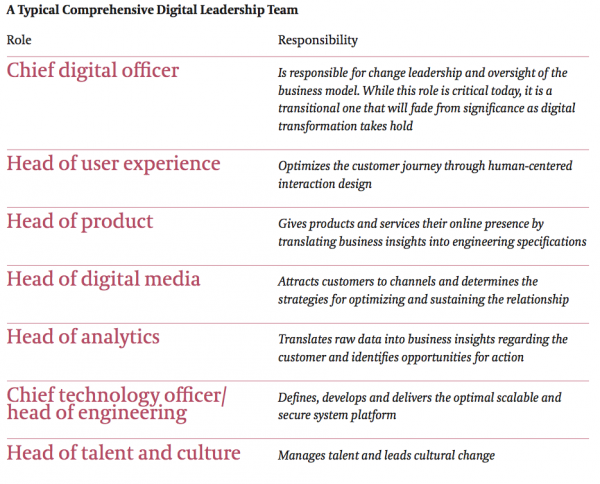

A team-based view of digital leadership. However digital talent is positioned within an organization, the responsibility for implementing digital transformation cannot rest on a single pair of shoulders. Not only is the task too great, but the field has matured into specialized subfunctions no one person can master. A successful talent strategy, therefore, must recruit and retain several types of digital leaders (see Figure 2).

A compelling pitch. Financial services firms will not succeed in attracting the people needed unless these companies are able to inspire a skeptical digital talent marketplace. Fortunately, they can do so with a winning vision and an obvious commitment from the top — if they express that vision and commitment in terms that will resonate with their audience. The opportunity to help disrupt the relationship between consumers and their finances is the sort of epic challenge to which digital leaders are drawn. Candidates will want to know that they will have the authority, budget and flexibility to hire the team they need. Candidates also will want to know that they will be measured in a way that reflects a winning philosophy: satisfied and engaged customers lead to a strong bottom line. Measuring these innovators by traditional finance-driven key performance indicators is likely to fatally undermine efforts to succeed. While candidates will expect that firms will have thought through organizational issues and reporting lines, allowing candidates to shape the role and the culture will strengthen their engagement with the opportunity (in addition to sharpening the job specification). Finally, ensure that the recruiting process is fast moving and high quality and, thus, is a tangible representation of the future it is hoped the candidate will help the company achieve. Including Executive Committee members on the interviewing team is a forceful way of demonstrating the importance a company places on digital initiatives.

A far-reaching search strategy. There is a shortage of proven digital leaders from within the financial services industry, but there also is a distinct need to bring in people with fresh perspectives, given that most financial services executives have been trained to look at products rather than customer experience. Financial services companies, therefore, must be prepared to reach outside their own industry for digital talent — an undertaking that requires deep insights and relationships across sectors and, because digital comes in many different varieties, the experience to compare candidates across contexts.

Companies headquartered in countries where there is regulatory involvement in senior appointments may have less leeway in hiring from outside the industry. In these countries, however, there has been a trend toward accepting non-financial services candidates with experience in high-availability and high- transaction volume systems, such as telecommunications, retail and travel.

A targeted assessment process. However much a digital executive’s technical knowledge and experience may be coveted, those who are able to lead on the path to digital transformation have a broader set of attributes as well. These attributes can be separated into competencies and potential to succeed in the face of the unknown.

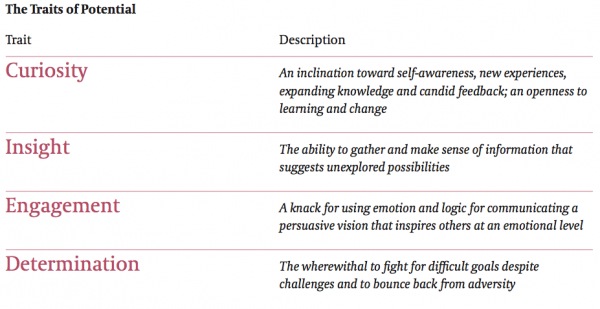

For more than a decade, screening for experience and competencies has been standard procedure for evaluating leaders (see Figure 3). But the underlying assumption in doing so is that future success can be accurately forecast from past performance — an assumption difficult to justify in today’s dynamic, complex, uncertain and ambiguous time. While competencies provide an important inventory of a candidate’s current capabilities, it also is critical to examine a leader’s potential to adapt to new and unknown conditions and acquire other competencies as the situation demands. By analyzing the career of thousands of executives, Egon Zehnder has identified four traits shared by leaders who have demonstrated such potential (see Figure 4).

A tailored integration process. Using a legacy onboarding process for someone being asked to lead a transformation will send mixed messages that undermine a new hire even before he or she starts. The overall onboarding framework must be rethought and should be determined by how the digital capability is distributed within the organization. But even when digital capability is woven throughout the enterprise, the task is as much to integrate the rest of the company with the incoming leader as it is to tie the digital capability back to the core of the company.

If promises were made in the recruiting stage regarding resources, streamlined decision making or other factors, this is the time to make good on those pledges. Like the recruiting stage, the onboarding process needs to be fast and efficient.

An aligned company culture. For the integration to take hold, the commitment to transformation must receive continual reinforcement from a company culture that is risk tolerant, adaptive, deeply empathetic for the customer and relentlessly focused on the customer experience. Unneeded roadblocks to innovation must be removed, with the understanding that there will be both successes and failures along the way. Decision making must be decentralized so that team members are empowered and a culture of collaboration can take hold. Incentives have to be aligned between legacy and digital individuals and teams to reinforce the fact that everyone is moving toward the same goal. Establishing an Innovation Advisory Board can help accelerate the process through the collective best practices of those who have been involved with similar initiatives elsewhere.

A unified technology delivery model. Financial services firms are notorious for the siloed nature of their data systems, as well as for their large-scale back-office technology operations. In today’s environment, this combination represents an unacceptable impediment, and organizations need to evolve to a model where business lines and the technology that supports them work together in an agile manner. The most innovative institutions have adopted the democratization of technology. They have understood that the future lies in open architecture and the ability to create a resilient and efficient technology platform while enhancing the data layer and enabling partnerships with the broader ecosystem for tailored application and services.

It is understandable for these tasks to seem daunting. After all, they reach to the very core of the organization and the value it offers customers. Financial services institutions navigating this transition can take solace in the fact that no one is immune — even digital pure-play organizations must contend with a hyper-competitive talent market and the necessity to continually refine their vision in the face of shifting customer expectations. Companies that fully embrace this digital undertaking, however, will be able to attract and retain the digital leaders required in today’s customer-led world and deliver an inspirational experience to customers.

Access the full paper Making the Future Now.