How can a leader dispel the myth that contrasting views are bound to clash? The answer lies in finding common ground. This valuable lesson stems from my recent conversation with Robert G. Eccles, an author, ESG expert, and Visiting Professor of Management Practice at the Said Business School at Oxford University.

Eccles's profound optimism and extensive background—he co-founded the International Integrated Reporting Council (IIRC) and served as the Founding Chairman of the Sustainability Accounting Standards Board (SASB)—have uniquely equipped him to navigate the polarized landscape of United States politics, particularly in the realm of sustainability.

Our engaging conversation left me inspired by his commitment to meaningful discourse, especially with individuals holding divergent viewpoints yet sharing concerns about critical issues. Throughout our interview, we explored the terrain of sustainability reporting, delving into the challenges and opportunities it presents to businesses, and examined the pivotal role of leadership in promoting bipartisanship and unity.

Read on for highlights from our conversation:

What sparked your interest in sustainability? Was it an evolution or was there an event?

It was an evolution. I've always been interested in measurement and became a professor at Harvard Business School. My research initially focused on topics like transfer pricing and investment banking. Over time, I shifted to corporate reporting, authoring articles where I saw the glimmers of sustainability reporting. I later chaired the Sustainability Accounting Standards Board, driven by a focus on what companies report, what investors want, and how sustainability affects businesses. This led to the International Sustainability Standards Board's (ISSB) formation. It's like a 30-year dream come true.

What's your outlook for the direction of travel, perhaps a destination, and the burden of reporting on corporates?

Sustainability reporting has evolved significantly, moving from voluntary reporting by NGOs—like the Sustainable Accounting Standards Board (SASB), Global Reporting Initiative (GRI), Climate Disclosure Standards Board (CDSB), Task Force on Climate-related Financial Disclosures (TCFD), and International Integrated Reporting Council (IIRC)—to a more structured framework. The creation of ISSB marked a significant shift, focusing on single materiality—factors that matter for enterprise value creation.

The landscape now includes the Global Reporting Initiative (GRI) emphasizing double materiality and the Corporate Sustainability Reporting Directive (CSRD) requiring sustainability reporting by European companies and those with substantial European business. Here the European Financial Reporting Advisory Group (EFRAG) has created the European Sustainability Reporting Standards (ESRS). While the U.S. Securities and Exchange Commission’s (SEC) proposed climate disclosure rule complicates matters in the United States, ISSB is seen as the global baseline, and the process, although complex with various personalities and politics, is crucial in advancing sustainability reporting.

However, standards alone won't solve all issues; while they enable investors and other stakeholders to compare performance on an “apples-to-apples” basis, corporate form (i.e., company law) and regulations also play vital roles in achieving sustainability goals. We'll see this emerge over time, but it'll always be a challenge.

Is there a moral component to measurement?

I distinguish between value-based investing and values-based investing. There's the ethical dimension, and then there's the question of whether companies are making the world a better or worse place while they're creating value. Should investors take a moral stance on companies that are making the world a worse place? That gets to be quite complicated because there's the fiduciary duty that the investors have to guarantee the returns for the beneficiaries.

But people are complicated, and if your beneficiaries have interests that go beyond pecuniary, and they want these things to be taken into account, then how does that get sorted out? There's a lot of complicated questions in the United States with the culture wars.

Can you give me some insight into your activities around bridging the divide that's in the US at the moment? Is it real?

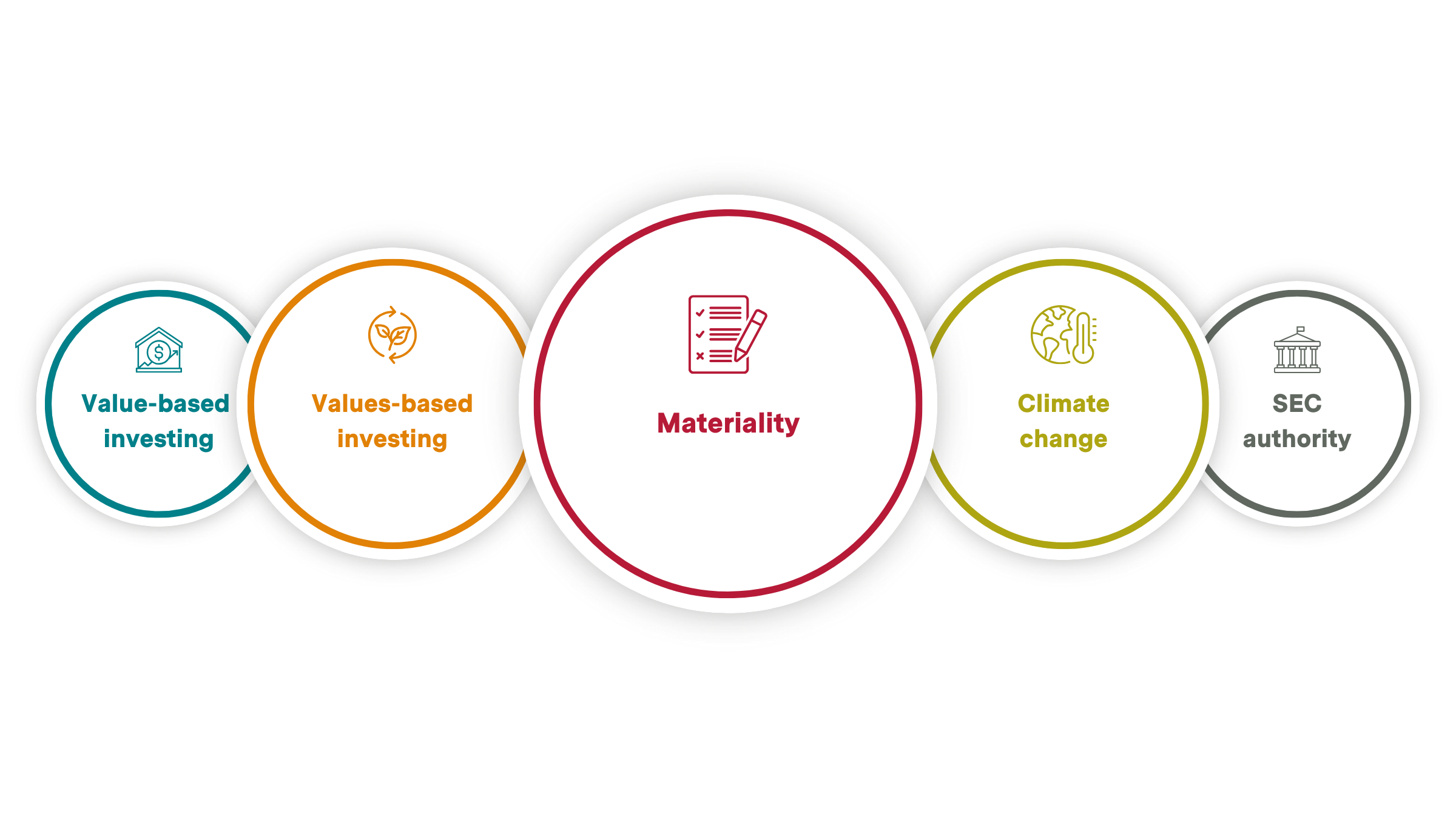

The U.S. is a very polarized country. The left's perception is that Republicans are all climate deniers, but they aren’t, and I've met a number of Republicans that are very concerned about climate change. Although I am a Democrat, I actively ask, ‘what are the grounds on which we can agree?’ And there's five sections: Value-based investing, values-based investing, materiality, climate change, and SEC authority.

I've found that discussions with politicians and their staff, away from the public domain, can lead to productive conversations. However, there's a need to consider the two levels of political theater and genuine understanding when assessing the ongoing culture wars. I've also highlighted the importance of evaluating the division of labor between the private and public sectors in addressing these issues.

I've co-authored articles such as "Turning Down the Heat in the ESG Debate” (with Dan Crowley), "Rescuing and ESG from the Culture Wars” (with Dan Crowley), “It’s Time to Take the Unnecessary Politics Out of ESG and Retirement Savings” (with Tim Doyle) and "It’s Time to Call a Truce in the Red State/Blue State ESG Culture War" (with Eli Lehrer). These efforts have revealed significant areas of agreement, like distinguishing between values-based and value-based investing and recognizing the importance of materiality. These are very easy conversations to have.

What is your sense of different parties who are in the system changing the system?

The prevailing narrative suggests that the public sector is failing, and the private sector must fill the gap, aiming for $2.5 trillion annually in capital. However, this notion is just a myth. In reality, there may be closer to $200 billion or $300 billion in feasible investments. Many of these opportunities are in developing countries, where challenges related to rule of law and project structuring are prevalent. Infrastructure investment is attractive due to its long-term cash flow potential.

The complex question at hand, with no definitive answer, involves establishing a global multilateral regulatory framework in a contentious global landscape. Different regions will adopt varying approaches, with Europe favoring more regulation, such as the Green Deal and EU Taxonomy. Global sustainability reporting standards are crucial, though not a panacea, and creating a global carbon pricing market could be beneficial. But again, whether it's the culture wars in the United States, whether it's kind of, Europe vs. the U.S. or it's the U.S. vs. China. There's always going to be differences, so where do you find those points of agreement?

What would be your advice to board members or potential board members on this topic?

I don't actually think it's that complicated at the board level. Focusing directors’ core responsibility, which is value creation of the corporation, there's five or six material issues that matter to value creation. And when you look at them, whether they are for a bank, pharmaceutical company, or an oil and gas company, they're all different and pretty sensible.

What board members really need is for management give them their point of view of what they think the material ESG issues are and articulate how they're related to financial performance. Is this about upside? Or downside? Is this revenue growth? Is it customer satisfaction? Is it higher gross margins? And then basically say, ‘OK, I understand where the ESG stuff fits into the mix of value creation.’

And then I think it's important for board members to be aware of other stakeholder concerns as to where there's these negative externalities that are being created. But again, what people have to accept is that there's trade-offs—you can do things that make a group that's concerned about a social issue happy, and it'll make an environmental group unhappy and vice versa.

What role can CFOs play in sustainability?

The CFO role has to expand beyond just the financial numbers and understanding how sustainability performance can affect financial performance and make this part of their discussion with investors. They need to form a view on the material ESG issues and what each one’s link is to financial performance. CFOs need to be aware of the different sustainability standards being developed and then develop tine internal control and measurement systems to report on them. evolved, actively engaging with investors and oversee internal control and measurement systems, aligning with ISSB standards and ESRS under EFRAG.

At the same time, Chief Sustainability Officers (CSOs) must become more focused on the truly material issues that matter to a company’s ability to deliver value over the long-term. They need to be able to explain the relationship between sustainability performance and financial performance and get more involved in discussions with investors. And they need to work closely with the CFO to develop the necessary internal control and measurement systems for reporting on sustainability performance.

In short, CFOs and CSOs need to become bilingual.

How do you define your purpose as a leader?

I consider myself a capital market activist, working within the existing system to mobilize capital respectfully, fostering discussions with individuals from various political perspectives. My purpose can be described as just four activities: creating content, presenting content, meeting people, and introducing people to each other. I am looking to drive system-level change, utilizing my reputation and network to find common ground across political divides and address issues of shared concern.

Who inspires you?

I have enormous respect for John Elkington, who has been a great leader on sustainability. Paul Polman, I would obviously cite. Steve Lydenberg too, on the investor side. He's always been the forefront and founded one of the first socially responsible investment firms, Domini Investments, and formed KLD Analytics, which is one of the first ESG data rating organizations. So, kudos to them.

It can be tempting to retain a strong position or float below the surface with a “green-hushing” position – it does take bravery to put yourself in the middle to hear and engage with all sides of an argument. I think Bob’s approach – ‘what are the grounds on which we can agree?’ – is a powerful initiation to conflict-ridden topics (even outside the Sustainability arena). To be “in the world” as a capital market activist, trying to find a way forward to change the system; knowing there is no “silver bullet” or immediate solution, it is tough and requires resilience to weather the backlash that is inevitable in social media and resilience to “just keep going” with conversations and connections.

Leaders at all levels are a vital component for delivering a positive outcome on the question “whether companies are making the world a better or worse place while they're creating value”. Board members, CEOs and Functional leaders are especially important for developing bi-lingual skills throughout an organization to deliver reporting, value-creation, innovation, culture and governance (to name a few) that fully integrate the breadth of the sustainability topic.